Monologue

We woke up this weekend to the grim news that America and its allies in the Middle East are at war with Iran.

The US and Israel launched missile strikes against Iran on Saturday morning. Unlike last year's targeted nuclear bunker attack, President Trump stated that the goal is open-ended this time ("eliminating imminent threats from the Iranian regime"). Iran retaliated with strikes on US bases in the region. Some of the world's busiest airports in the Gulf are shut down. As we go pens-down, unconfirmed rumors that Iranian Supreme Leader Ayatollah Ali Khamenei has been killed are circulating, opening the possibility of a major leadership vacuum (although head of government President Masoud Pezeshkian appears still to be in charge).

I'm not a geopolitical analyst, so I won't prognosticate on the likely course of events just yet, nor evaluate the strategic value of a strike. There are still too many open questions (e.g., whether either side is open to de-escalation, whether ground troops could be involved, how the Iranian public is reacting).

I will point out that this action is in line with our guidance that Trump is stalemated on domestic policy by the midterms and markets, and therefore more volatile on the global stage. This principle should guide our medium-term (i.e., remaining Trump years) thinking regarding the US.

I do have a remit to comment on the economics of the situation. From that standpoint, as significant as the strikes feel, this war is unlikely to have much of an impact on the global economy. This is not the 1970s. Iran has been excluded from the global economic system by years of strict sanctions and is not a leading oil supplier, so the possible impact is limited to a blockade on oil shipping through the Strait of Hormuz to the UAE, Saudi Arabia, Kuwait and Iraq — in the context of an already oversupplied market.

We're not staring down the barrel of a stagflationary shock via the oil price. Futures markets only rose by about $2 per barrel on Saturday, with analysts predicting a potentially more significant but still manageable $5-10 jump when markets reopen on Monday.

To be sure, a sustained conflict is yet another upward inflation risk to add to the list, but it does not change the game.

That brings me to the topic I had originally planned for this week's monologue: the risks to the "Goldilocks" regime that the US economy has entered (higher growth, stable (for now) inflation, easy financial conditions). See last week's note for details.

A crucial component of our model's assessment of the current US economic regime is stable prices, which it's picking from various inputs – most notably soft core CPI in December and January, and some survey data that reflect businesses' tariff cost fears were not as high as feared in mid-2025 (though forward-looking plans to raise prices remain in place).

Accordingly, the biggest risk to the "Goldilocks" regime is rising inflation, which would put the economy into an "Overheating" regime (good for asset prices in the short term). On the latest data, our modeling puts the odds of this transition in the next 12 months at 10%.

There are a few things that the data we feed the model aren't yet capturing. These include the Iran war, tariff-related markups, immigration restrictions tightening labor markets further, and AI investment bottlenecks, all of which lead me to put that probability closer to 25%.

A related problem is that the Fed has talked itself into a position where raising rates in anticipation of rising inflationary pressure will be very difficult to pull off, at least in the next 6 months or so. The narrow window to head off an inflation spike may be missed, sending us into a cycle of overheating followed by financial repression – a replay, on a smaller scale, of post-COVID-19 dynamics.

A few other things to note:

- AI is both a "Goldilocks" support (driving investment and potentially productivity gains) and risk, should that lead to bottlenecks.

- Related, a major equity crash of the dotcom variety remains the most important tail risk. Even if that were to occur, we see it a year or two out (these things are always later than predicted).

- Private credit stresses and wider default concerns could do the Fed's work of tightening financial conditions by themselves.

On that subject, I should point out that there is a relatively long commentary on the nervousness around private credit in the Market Monitor, so this is a good place to leave the Monologue.

Dylan Smith

Founder and Chief Economist

Marginal

Rising 👆

- Insider Trading: Hidden alpha — "We provide novel evidence suggestive of insider trading through concealed relationships identified using information from over 100,000 Facebook profiles and their 35 million friends[...] These hidden ties emerge as the most powerful predictor of future stock returns among documented network characteristics, with predictive power increasing over time through the present day."

- R-Star: The Post‑Pandemic Global R* — "After declining significantly from the 1990s to before the COVID-19 pandemic, global r* has risen but remains well below its pre-1990s level."

Falling 👇

- Open-ended funds: The problem isn’t democratizing private markets. It’s confusing access with liquidity — "The Blue Owl episode shows that even when managers behave exactly as they should—and are incentivized to—the structural fragility of placing retail investors into illiquid assets has real implications."

- Hiring fears: McKinsey, Bain Rush to Hire College Interns Before Big Banks Do — "McKinsey & Co. has pushed forward its recruitment timeline for next summer’s crop of college interns, the latest salvo in the war for talent among top consulting firms and Wall Street." And Private Markets Hiring Defies Gloom With $2.5 Million Pay Deals.

Macro Monitor

There was little in the way of interesting new macroeconomic data this week, with only one real data point of note for the US. That was Friday's January Producer Price Index report, which showed core prices up a whopping +0.8% on the month – a huge surprise to the +0.3% expected by the forecast consensus.

Inflationary pressure is not fading.

North of the border, Q4 GDP data for Canada confirmed that trade tensions are a major drag on growth at present, masking a pickup in spending and investment.

See the appendix for arcMacro proprietary Factors and the Key Macroeconomic Indicators tracking chart.

Market Monitor

Public markets

The price of WTI crude oil only ticked up by a dollar per barrel as US-Iran tensions ratcheted up this week, closing at $67.3 per barrel on Friday evening. Forward prices are up by another ~$2 per barrel on Saturday as markets try to digest how long the Strait of Hormuz will be effectively closed to shipping, whether regional production outside Iran is at risk, and how that tallies against an otherwise oversupplied market.

Gold rose by 3% this week and will likely have another bumper rally over the coming week (setting up selling opportunities for those rebalancing holdings?). Safe haven demand was evident too in a strong Treasuries rally, which took the closing yield on the 10-year Treasury Note below 4.0% for the first time since October 2025, and before that, October 2024.

So much for "dollar debasement."

The song remains the same in equities, with averages little moved amid a giant rotation from software and services into real cyclical stocks.

This week, the dynamics took on a surreal tone, with the strange phenomenon of a Substack-disseminated thought experiment on AI's impact on the economy triggering a massive sell-off. Citadel Securities' well-timed response was on-point, so I'll refer you there rather than rebut Citrini Research directly.

One way of looking at momentum in the market suggests that software is due a bit of a rebound:

Private Markets

Misunderstanding private credit

Markets appear to have cottoned on to the fact that the lower interest rate environment (compared to 2022-2024) is bad for private credit, since its main advantage over traditional credit structures is a floating-rate structure with strong, deal-specific covenants.

Private credit's main pitch to investors when the Fed was tight was essentially that it was stepping in to provide much-needed liquidity to the economy, charging high rates to do it, and was willing to accept higher default risk as a result.

As the Effective Fed Funds rate has come down from the peak of 5.3% to 3.6% now, that default risk has become proportionally more important, especially in weaker pockets of the economy. The hype around private credit took too long to cool as its value proposition weakened, and has now flipped suddenly into active fear.

Enter Blue Owl, which was in the market's crosshairs this week, at the center of a broad selloff in publicly listed private markets investment firms. The more involved a listed manager is in private credit, the more they have fallen. The skepticism was triggered by Blue Owl's decision to block redemptions from an open-ended credit fund (OBDC II), and instead accelerate liquidations to return cash to investors.

In our view, the fears are a little overblown. For one thing, defaults happen even in the best of times, and Blue Owl is basically doing what they're supposed to (prioritizing a sale at book value to return cash rather than allow the fund to come under deeper pressure).

For another, lending is senior to equity exposure and private credit uses extremely tight covenant agreements. To take the example of private lending for data center construction, if you're worried about overbuilding, why not focus on the equity providers – the hyperscalers themselves?

Blue Owl's situation highlights another difference between private credit and public credit: private credit risk is concentrated, not diffuse, making it less systemic. According to the Alternative Investment Management Association (AIMA), 80% of private lending happens in closed-ended private-equity-style vehicles.

In these funds, losses stop at the institutional investors in the fund. OBDC II is in trouble partly because it is in the minority of retail-focused open-ended funds, with redemptions rising at exactly the wrong time from the fund manager's perspective.

The lesson is not that systemic default risk in private credit is to be feared; it's that providing liquid access to illiquid investment vehicles may be a flawed idea. Blue Owl is not alone in struggling to square this liquidity mismatch challenge. Just recently, open-ended real estate fund Trez Capital suspended redemptions, and an example in midmarket PE is Toronto-based Kensington Capital Partners.

To sum up, private credit is being hit for the wrong reasons. What we're seeing play out is a business model challenge that is in part cyclical (lower interest rates eroding absolute returns and competitive advantage) and in part structural (open-ended funds). The cyclical factor will drive lower-than-promised returns (there is no private free lunch), but not catastrophic failure. The structural issue suggests we might need to pump the brakes on the "democratization" of illiquid funding structures.

Final aside: if the major sophisticated private markets investors are pension funds, is this asset class not already highly democratized?

Battle of the outlooks

Bain & Company has put out its Global Private Equity Report 2026, hot on the heels of McKinsey (which we linked last week).

We shouldn't forget that these reports are at least to some degree window-dressing. Still, we can learn a lot about the key sources of uncertainty in the PE world by comparing the two reports.

Where they agree: Unsurprisingly, both agree on the important features of the status quo, notably low distributions and an historic backlog of unsold companies, high entry multiples, and a nascent, megadeal-driven recovery. LPs are keeping allocations stable, but concentrating on a more selective set of funds.

Where they differ: Bain is more bullish. There are some framing differences – Bain casts the past three years of PE return underperformance more as public benchmark anomaly than a problem with private assets per se. Bain sees 2026 as primed for an upswing in deal making, and expects top-quartile funds to outperform public markets, while McKinsey expects further IRR compression across the board amid a more demanding deal environment. Both expect the pressure to re-raise funding will lead to a pickup in failure rates, with Bain placing the number at 20% (15% being "normal"), seeing the "Zombie" discussion as overblown, while McKinsey strikes a more watchful tone.

Our take: We're a little closer to Bain. Our emphasis is on how the macro environment shapes decisions by private markets operators. We see conditions shifting in favor of stronger operational growth and valuations for a broader set of portfolio companies, helping to accelerate exits and improve distributions. This puts us in the early phase of a 3-5 year capital renewal cycle.

See the appendix for the market monitor table

Memo

The tides and currents of the PE cycle

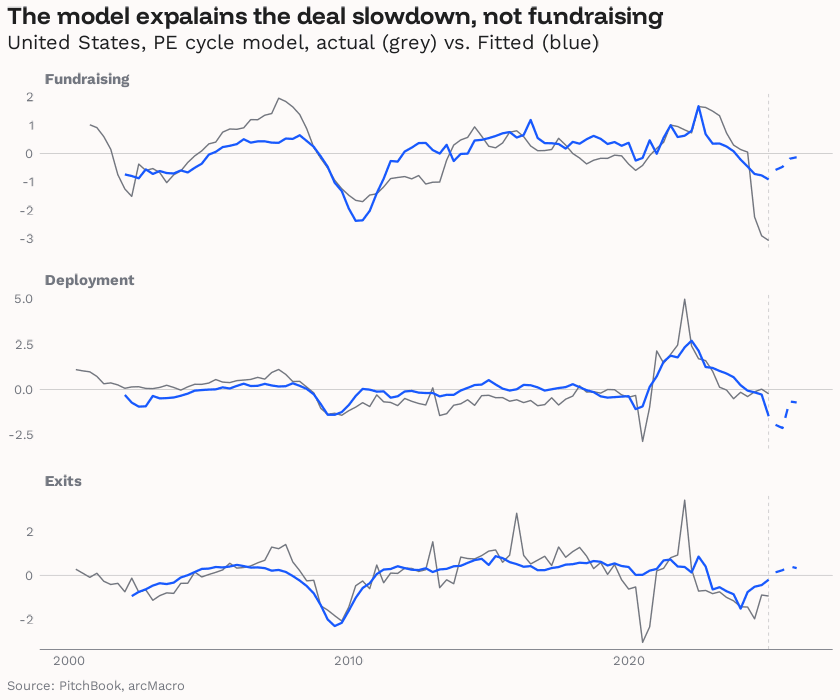

Bottom line: Private equity activity follows a predictable cycle driven by the state of the economy (the "tides" of activity and financial conditions) and prior PE activity ("currents" created within the sector itself). Our modeling suggests that waning currents and rising tides should drive exit counts above trend this year.

What it means for businesses and investors: The reason for PE's slump in the past several years is a natural consequence of weak macro conditions and the hangover from the 2020-2022 sugar rush. With macro conditions entering a "goldilocks" phase and time moving on, exits are ready to pick up in 2026, setting the stage for fundraising conditions to improve in 2027.

The classic private equity (PE) buyout fund lifecycle consists of three sequential stages. In the fundraising stage, funds are launched by general partners, and commitments (funding) made by limited partners (LPs). In the deployment stage, the GP identifies target companies, calls its capital from LPs, makes its investments and gets to work growing the value of its portfolio. In the final exit stage the GP sells its portfolio holdings and returns cash to LPs (disbursement).

For most GPs, these stages are sequential. One can't do deals without first securing funding, nor exit those deals without making them in the first place. It's cyclical too: new fundraising depends on successful, high-return exits from prior investments.

This piece is about understanding why we observe a similar pattern on the aggregate level. If each GP launched its fund at a random time and followed the cycle above, aggregate fundraising, dealmaking and exit activity would not show any cyclical pattern over time.

The fact that it does tells us that something else is driving PE activity and creating conditions that the entire industry reacts to.

The table below shows that there is moderate positive correlation between the three phases of the PE cycle on aggregate — but only moderate. The components of the PE cycle are not perfectly in sync with each other.

Looking at the correlations between PE activity and two of our arcMacro Factors – the Real Factor telling us the state of activity and economic growth, and the Financial Factor signaling how easily firms can access funding – is instructive. It suggests that:

- All stages of the PE cycle demonstrate significant correlation with underlying macro factors.

- Real activity and financial conditions are separate channels.

- Fundraising builds with lags: sustained strong activity and easy financial conditions are needed to drive funding into private markets.

- Deployment is highly sensitive to real activity and leveraged to the growth outlook.

- Exits differ from deployments – they depend on financial conditions, which drive M&A levels (through financing availability) and IPOs (a valuation story).

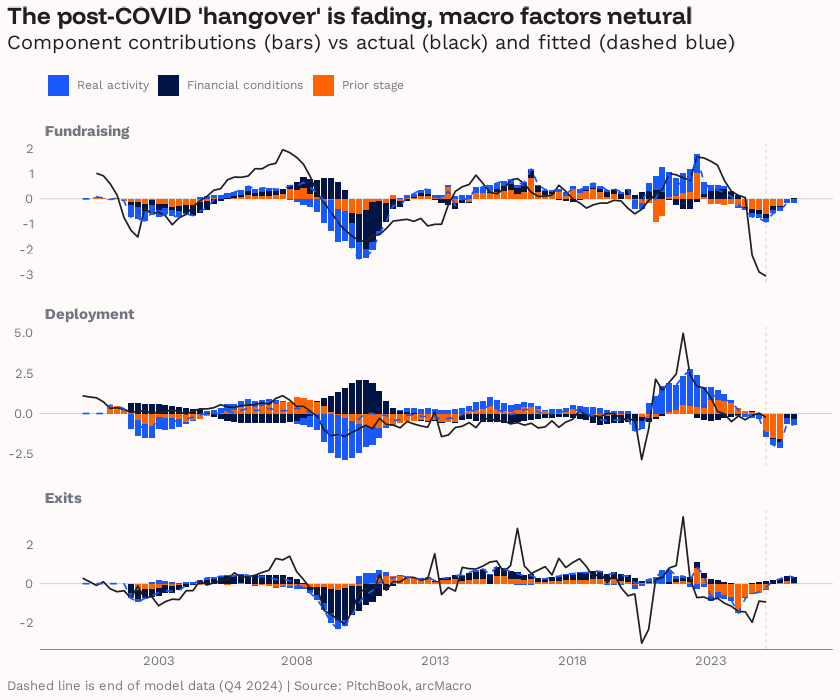

We can formalize and deepen those insights with a few regressions. We model each phase of the activity cycle – funds launched, deal count (deployment) and exit count, as a function of the optimal lag of the prior phase, and current and year-ago Real and Financial factors.

For example, fund count depends on the number of exits six months ago (capital recycling), and the state of the real economy and financial conditions (both reflecting expected returns and risk appetite).

A few technical notes for those interested (skip this paragraph if you're not). These data are seasonally adjusted, de-trended and z-scored, giving the "cyclical" component of PE activity. Raw fundraising data exhibited an exponential pattern and was logged before detrending. Each equation contains five parameters in a quarterly sample with over 90 observations spanning the period 2000-2024. Diagnostic testing showed some evidence of serial correlation, so robust Newey-West standard errors are reported.

With that out of the way, here is what the regression table tells us:

- The model explains about half of the quarterly cyclical movement in PE activity — R-squared statistics are high without being spurious (0.42–0.52). For a simple model of a volatile and "lumpy" industry, that's a striking success.

- Cyclical industry momentum matters — lagged activity in the prior phase of the PE cycle is significant for all models.

- The macro drivers affect the stages differently — fundraising responds to real activity and lagged financial conditions, deployment is sensitive to all macro inputs, and exits are about financial conditions.

- The congestion effect in exits is structural — more deals 8 quarters ago means fewer exits today. Heavy deployment creates exit queues in the form of supply-side crowding that suppresses exits ~2 years later.

- Recycling is an aggregate phenomenon, too — A one standard-deviation rise in exits causes a 0.3 standard deviation rise in fundraising two quarters later.

Looking at the model's predicted values against the actual cyclical component of PE activity shows that our framework does indeed explain things quite well — with the exception of some timing differences around COVID-19 (no surprise) and the drop in fundraising in 2023/2024, which has been more extreme than anticipated.

We can decompose those predicted values to disentangle the two main effects driving the model – how each stage of the cycle is driving the next stage, and how macroeconomic conditions are influencing activity.

The results are extremely informative. While the "sluggish" macro conditions over the past three years have certainly not helped matters, the PE industry has been in a state of cyclical depression because of its internal dynamics. The (macro-driven) surge in activity during the COVID-19 recovery severely restricted future activity, putting the industry in a holding pattern.

The good news is that this effect is now fading. As of the end of 2025, macro factors have turned marginally positive and the hangover is coming to an end.

Our modeling suggests that exits will tick back above the historical trend this year, with an improvement in fundraising 6-18 months behind. Deployment will stay roughly at trend for the time being.

This model is obviously not complete. It does not account for the buildup of dry powder or explain hold length, both of which would help explain recent deviations from predicted values and nuance the forward-looking predictions of the model.

But, it's surprisingly powerful, and a good enough start to convince us to take a deeper dive in the form of a forthcoming Special Report.

Stay tuned!

Appendix

Proprietary Factor and Regime Model and Key Macro Indicators